Part III of a three-part series examining the economic fallout of the West Asia conflict on India. Here's Part I and Part II

India’s chief economic adviser V. Anantha Nageswaran on Tuesday termed the ongoing West Asia crisis a “live balance of payments stress test”, with rising crude oil prices and a weakening rupee set to widen India’s external imbalances, putting pressure on both the current account and overall balance of payments in FY27.

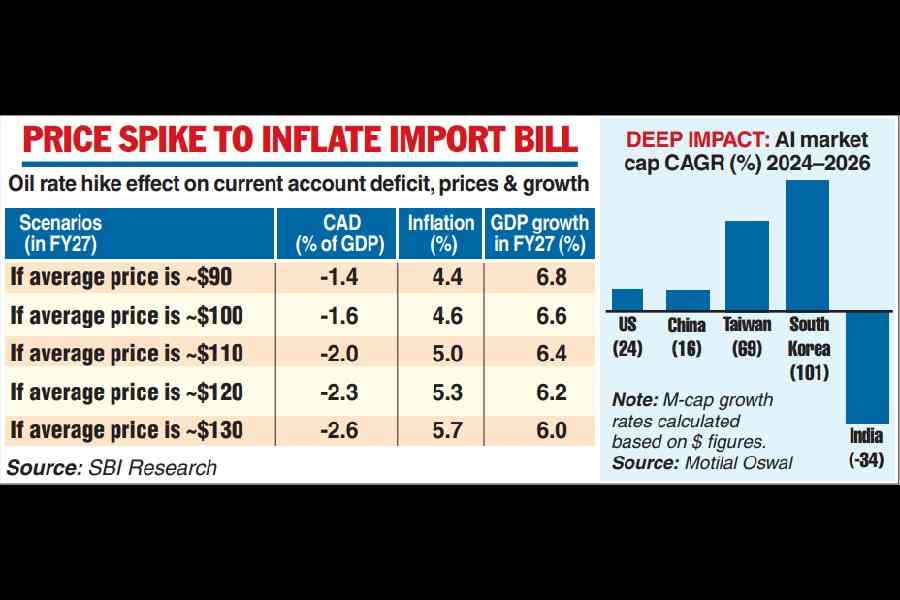

Economists warn that a sustained spike in energy prices could significantly inflate the import bill. “Amid ongoing geopolitical tensions, elevated oil prices are likely to persist, leading to a deterioration in the current account due to a higher oil import bill, along with gas-related disruptions,” said Upasana Chachra, chief India economist at Morgan Stanley.

She added that the sensitivity to energy prices remains high. “With oil prices averaging around $95 per barrel, we now expect the current account deficit to widen to about 2.5 per cent of GDP in FY27, compared with our earlier estimate of 1 per cent, which assumed oil at $65 per barrel,” Chachra said.

Other economists, however, see the deterioration as manageable. “The current account deficit is likely to widen to around 2 per cent of GDP, which remains within manageable levels,” said Gaurav Kapur, chief economist at IndusInd Bank.

He pointed to structural buffers that could help cushion the impact. A growing services trade surplus is expected to offset part of the widening merchandise trade gap, while an interim trade agreement with the United States and recently concluded free trade agreements could help mitigate external demand risks arising from disruptions in West Asian export markets.

However, pressures are likely to persist on the capital account. “The balance of payments could remain in deficit in FY27, in the range of 0.5–1 per cent of GDP, driven by another year of net foreign portfolio investment outflows. That in turn would mean the rupee will continue to trade with a weakening bias,” Kapur said.

Inflection point

India’s IT services sector—long a key driver of export earnings and foreign exchange inflows — is entering a more uncertain phase, caught between shifting global demand dynamics and the disruptive impact of artificial intelligence. This is expected to put pressure on the balance of payments.

The demand environment has softened, weighed down by US tariff risks and cautious technology spending by global clients. At the same time, AI-led productivity gains are beginning to compress revenues in legacy services, while also dampening hiring momentum across the industry.

Investor sentiment has also turned more selective. India’s relatively lower exposure to the global AI rally has meant it has lagged key markets. Data compiled by Motilal Oswal Financial Services shows that the market capitalisation of Indian IT services firms has contracted at a compounded annual rate of 6 per cent since 2022, compared with gains of 43 per cent in the US, 57 per cent in Taiwan and 33 per cent in South Korea — largely driven by an AI-linked rally.

The impact is increasingly visible on the ground. Top IT firms collectively reduced headcount by around 7,000 in FY26, signalling a shift away from the sector’s traditional labour-intensive growth model.

Praveen Kumar, fund manager at AlphaGrep Investment Management, said the most meaningful challenge to the growth trajectory in the medium term could stem from IT services. “IT services are a huge part of our exports, and that helps us offset the deficit that we run as an economy,” he noted, adding that if IT services revenues stagnate or taper, it could have knock-on effects on both the current account and consumption.

“Data from listed firms, trade bodies and employment portals indicates that white-collar job growth has slowed to almost zero over the past three years,” said Saurabh Mukherjea, founder and chief investment officer at Marcellus Investment Managers.

The ripple effects are spreading beyond the sector. “This slowdown is weighing on residential real estate demand, particularly in tech hubs such as Hyderabad and Pune, where concerns around job security are affecting sentiment among IT and call centre employees,” he said, adding that industry leaders have been candid about the need for leaner workforces.

The structural challenges extend to the broader labour market. With around 80 lakh graduates entering the workforce each year and limited incremental demand, real wages — adjusted for inflation — have been declining by about 5 per cent annually over the past decade.

Yet leverage patterns tell a different story. “In an era of social media-driven aspirational spending, the middle class has taken on significantly higher leverage to sustain consumption levels despite falling real incomes,” Mukherjea said. “Non-mortgage household debt has trebled over the past six years. As we highlighted in our book Breakpoint: The Crisis of the Middle Class & The Future of Work, middle-class Indians are now among the most indebted globally,” he added.

Elevated bond yields

India’s 10-year government security bond yield, which was hovering at around 6.6 per cent before the West Asia crisis broke out in February, rose sharply to around 7.1 per cent in early April and is currently near 7 per cent.

Higher yields increase the cost of borrowing for companies, reduce the attractiveness of equities, and divert capital toward safer government debt. This is often driven by high government borrowing, which leaves less capital available for private sector expansion.

“The bond yields have been elevated, and the challenge for the monetary policy is that the situation cannot be addressed with a policy rate action. A cut in policy rates is not going to help in supporting demand, given the risk aversion of the businesses in such a scenario and the general weakness in consumer sentiment. The policy measures have to be targeted towards ensuring liquidity and credit availability for the MSMEs,” said Ranen Banerjee, partner and leader, economic advisory services at PwC India.

Tariff uncertainty

Global trade tensions are back in focus, adding another layer of uncertainty for Indian exporters. US Treasury Secretary Scott Bessent has indicated that tariffs — recently struck down by the US Supreme Court — could be reinstated as early as July by the Trump administration.

The potential return of tariffs comes at a sensitive juncture, with Washington expected to initiate fresh Section 301 investigations into multiple trading partners, including India, over concerns related to excess capacity. Key export-oriented sectors such as steel, textiles, pharmaceuticals and electronics could come under scrutiny.

The move also risks injecting fresh friction into bilateral trade ties at a time when both sides are engaged in negotiations aimed at reaching an interim trade agreement.

Market participants warn that sector-specific vulnerabilities remain elevated. Any escalation in trade barriers — or delays in securing favourable trade terms — could weigh on exports, which have already been navigating a challenging global demand environment.

In conclusion, Rudra Chatterjee, managing director of Luxmi Group, said that while geopolitical turbulence is reshaping the economics of growth through energy volatility, freight disruption and the concentration of AI capital and infrastructure, India’s response must reduce the energy intensity of growth through logistics and infrastructure, revive middle-class consumption through higher disposable income, expand labour-intensive exports, and ensure India becomes a builder, not merely a consumer, of global AI infrastructure and applications.