Part II of a three-part series examining the economic fallout of the West Asia conflict on India. Here's Part I

Prime Minister Narendra Modi’s appeal to curb foreign exchange outflows has underscored the mounting economic toll of the West Asian conflict on India, with policymakers increasingly concerned that a prolonged surge in crude prices could feed into broader inflationary pressures.

The impact is likely to be felt most acutely by households if state-run fuel retailers are forced to raise petrol and diesel prices, pushing up the cost of everyday goods and transport across the economy.

Inflation

India’s inflation story, which has largely stayed within the RBI’s comfort zone of 4 per cent (±2 per cent) in recent years, may be approaching a more turbulent phase.

Two risks are now converging. First, crude oil prices remain stubbornly elevated, threatening to feed directly into fuel and transport costs. Second, the India Meteorological Department’s forecast of a below-normal monsoon for 2026 raises the spectre of a food price shock. A weak kharif season could push up prices of pulses, cereals and vegetables, squeeze rural incomes and add a domestic supply-side layer to already building global pressures.

“There is a prediction of El Niño, and the IMD has forecast monsoon rainfall to be 8–10 percentage points below the long-term average. The impact, however, will hinge on how the rains are distributed and the incidence of extreme weather events, which tend to damage crops more than a simple shortfall — especially now that irrigation coverage has expanded across states,” said Ranen Banerjee, partner and leader, economic advisory services at PwC India.

He added that while food price risks are clearly elevated, comfortable foodgrain stocks provide the government with room to intervene if prices spike sharply.

For now, policymakers appear inclined to stay cautious. Economists expect the Monetary Policy Committee to hold rates steady in the near term, extending its pause as it assesses evolving risks.

“The MPC is likely to continue with a wait-and-watch approach at least until August. Some calibrated tightening could follow, with the repo rate potentially rising by about 50 basis points over the next 12 months,” said Gaurav Kapur, chief economist at IndusInd Bank.

Even so, inflation is expected to drift above the central bank’s target. “CPI inflation is projected to average around 5 per cent in FY27, which would erode household purchasing power and likely prompt rate hikes in the second half of the year,” said Devarsh Vakil, head of research at HDFC Securities.

Oil remains the biggest wildcard. “Every $10 per barrel increase in crude can lift inflation by about 0.5 percentage point. A 30–40 per cent rise in oil prices could, therefore, add 1.5–2 percentage points to inflation,” said Aditya Khemani, fund manager, Invesco MF.

Fiscal pressure

The government has rolled out a multi-pronged fiscal and regulatory response to cushion the economic shock from the escalating West Asia crisis. Key measures include a ₹1 lakh crore economic stabilisation fund, excise duty cuts on petrol and diesel, reimposition of export levies on aviation turbine fuel (ATF), and an expanded Emergency Credit Line Guarantee Scheme with a fiscal outlay of ₹18,000 crore. In addition, a Resilience & Logistics Intervention for Export Facilitation (RLIEF) package has been approved with an initial outlay of ₹497 crore, aimed at supporting exporters facing supply chain disruptions.

Even as these buffers provide near-term relief, economists warn that a prolonged conflict could stretch public finances and push the fiscal deficit beyond the FY27 target of 4.5 per cent (based on the 2022–23 series).

“The fiscal will come under stress primarily due to the sharp increase in global fertiliser prices, which will translate into a higher subsidy burden. At the same time, the decision to hold back increases in retail petrol and diesel prices will squeeze the margins of oil marketing companies, reducing the dividend income that the government receives from them,” said Banerjee.

He added that additional support measures for export-oriented sectors and MSMEs, coupled with a likely slowdown in demand impacting GST collections, could further widen the fiscal gap. “Under these circumstances, a deviation from the fiscal deficit target in FY27 would not only be likely but also warranted, as the government steps in to stabilise the economy,” Banerjee said.

Echoing similar concerns, Aditi Nayar, senior vice-president and chief economist at Icra, pointed to the multiple channels through which elevated crude prices could strain government finances.

“Sustained high crude oil prices could compress corporate margins — including those of oil marketing companies—thereby weighing on corporate tax collections. The recent excise duty cuts on fuels will also dampen indirect tax revenues in FY27,” she said.

At current crude levels, OMCs could face significant under-recoveries if retail fuel prices remain unchanged, further reducing dividend payouts to the government. “Additionally, the fertiliser subsidy bill could overshoot the budgeted estimate of ₹1.7 trillion in FY27,” Nayar noted.

While the government has moved swiftly to shield households and businesses, the cost of that protection is likely to show up in the fiscal math. If global commodity pressures persist, maintaining the glide path on deficit reduction could become increasingly challenging.

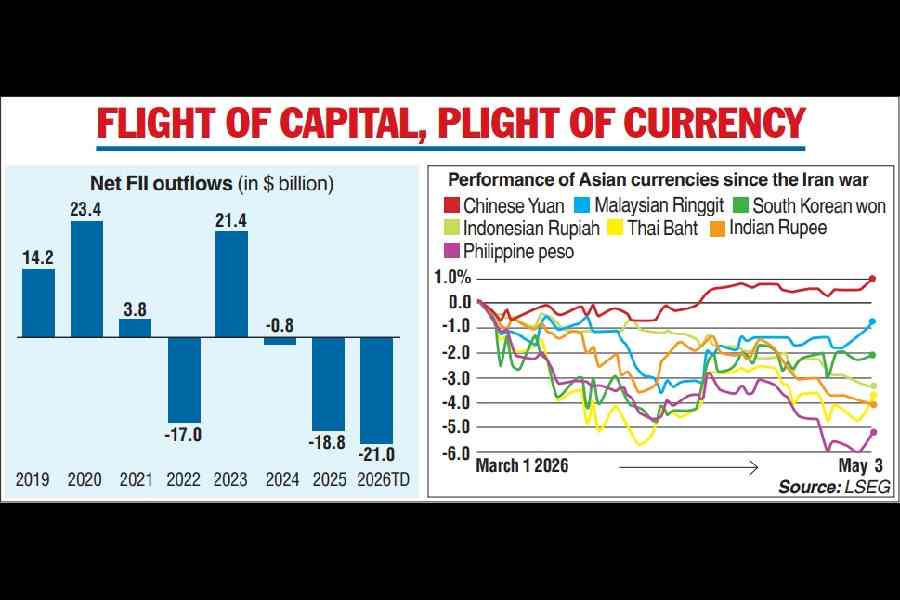

Rupee fall & FII outflow

Foreign investor sentiment towards India has turned sharply cautious in 2026, with cumulative outflows already surpassing last year’s total. Overseas investors have pulled out about $22.17 billion so far this year, exceeding the $18.9 billion recorded in all of 2025, underscoring the scale of the shift in capital flows.

The exodus has coincided with a sharp rise in crude oil prices, compounding pressure on the Indian currency. The rupee has weakened to record lows of around ₹95 per US dollar in early May, marking a depreciation of over 5 per cent since the start of the year. The Reserve Bank of India has stepped in with measures to curb speculative activity in non-deliverable forward (NDF) markets, helping to temporarily stabilise the currency. However, analysts caution that underlying pressures remain intact.

“The rupee has to become the shock absorber,” said Sajid Chinoy, chief India economist, JP Morgan. “There’s no magic solution. Either you run down reserves aggressively or allow the currency to adjust.”

He also pushed back against the idea that a strong currency necessarily reflects a strong economy, noting that many export-driven Asian economies historically relied on competitive exchange rates during high-growth phases.

“Over the last 18 months, we have seen significant FII outflows. The recent surge in oil prices has further weakened the economy, which, from an FII’s perspective, reduces the attractiveness of the Indian market,” said Khemani. He noted that the currency weakness itself can reinforce the trend. “A depreciating rupee lowers returns for foreign investors in their home currency terms, setting off a negative feedback loop that could prolong outflows,” he added.

“The valuations were high in the Indian markets, and other Southeast Asian markets were more attractive with their valuation levels. This has accelerated the portfolio outflows,” said Banerjee.

He added that higher crude prices, along with potential risks to remittance inflows from West Asia, are further weighing on the rupee.

The implications for the broader economy are significant. “Sustained outflows drain equity markets, weaken the rupee further, raise the cost of capital for Indian corporates and dampen market sentiments,” said Vakil.

To be continued