The unified payments interface, or the UPI, is the new boy in the payments market and has the makings of a blockbuster.

The biggest draw for the UPI is its ability to make payments seamless and instant by requiring the payee to only remember a virtual payment address (VPA), much like sending an email.

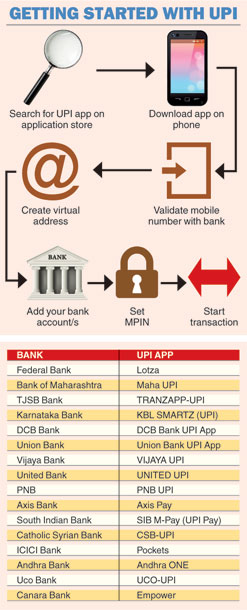

What is UPI?

The UPI has been launched by the National Payments Corporation of India (NPCI) to take forward the Reserve Bank of India's vision of migrating towards a "less-cash" and more digital society.

The UPI ecosystem functions with the following three key set of players:

• Payment service providers (PSPs), who will provide the interface to the payer and the payee. The interoperability will ensure that, unlike wallets, the payer and the payee can use two different PSPs.

• Banks, which will provide the underlying accounts for the payer and payee. In some cases, the bank and the payment service providers may be the same.

• NPCI , which will act as the central switch to determine the virtual payment address, effecting credit and debit transactions through the immediate payment service platform and settlement of funds across banks.

How does it work?

The UPI is a unique interface, which works 24x7 across the banking system and is instant, safe, secure, cost-effective and convenient to use.

The UPI will allow you to make payments directly from your bank account - so you don't need to pre-load your money in wallets that does not pay interest on the balance.

The UPI will allow you to pay different merchants without the hassle of typing your card details or netbanking password.

The UPI is built on top of the immediate payment service platform, which we have used to instantly transfer money between accounts with different banks.

All money transfers with the UPI are secured with a two-factor authentication (2FA) as mandated by the RBI - the first factor being your phone and the mobile PIN the second.

The UPI is capable of peer-to-peer transfers as well as peer-to-merchant transactions, including the option for merchants/service providers to ask for money.

Is it better than cards?

The UPI works on the unique idea of a "virtual payment address (VPA)" - which is something like "rajiv@axisbank". You only give the merchant your VPA, who can initiate a payment request against this unique ID. They can never get to see your bank account number.

The UPI can also be used for shopping online - instead of entering your debit card number, expiry date and the CVV code followed by waiting for the OTP, you have to just enter your UPI ID, and get an alert on your phone to verify the transaction.

Will UPI succeed?

Banks such as Axis Bank, which have almost half of its branches in semi-urban and rural areas, are witnessing more than 50 per cent of the transactions through digital channels and growing at over 30 per cent every year. This clearly shows that the customer is ready to go digital, provided the banks innovate and offer customer-centric solutions.

The UPI will make the payments system fully inter-operable across all players.

The launch of the UPI will usher in low-cost, high-volume payments and create a new ecosystem where customers and merchants will come together for faster and simpler electronic payments.

The UPI is likely to benefit the overall payments ecosystem as the service can be provided by banks to merchants with an entry-level smartphone and there is no need to install POS (points of sale) machines at the place of business.

Thus, it is likely to reduce the overall merchant acquisition cost for banks by providing a solution to the merchants that is mutually beneficial and have long-term benefits.

The most important aspect of the UPI is its open architecture. With the UPI, banks are free to innovate on the user experience as they feel is necessary.

The user interface is fully flexible and banks are free to create an intuitive interface.

We have seen time and again that when players are free to innovate, customers invariably get the best products and the acceptance of the products is far better.

This innovation will also bring all the key stakeholders such as the consumer, the merchant and the banks on a common platform, creating a plethora of services that are unheard of in today's global payment offerings.

All should join

The success of the UPI depends on the adoption of the platform by all banks in the country, which will ensure that an user can transfer money to any account of his choice.

Further, the user needs to have a smartphone to effect the transfer and, hence, the potential user base will be restricted to around 250 million people at present.

Parallely, on the acquiring front, there needs to be an aggressive push from the payment service providers to maximise newer merchants to popularise the UPI as a payment option.

With the way the payment industry is shaping up, we are seeing a burst of new technologies such as contactless payments ( near field communication or NFC), host card emulation (HCE) and tokenisation that make payments simple for consumers without compromising security. All of this could provide good competition to the UPI.

The writer is executive director, Axis Bank