|

A dispute between health care providers and public sector health insurers over the pricing of medical procedures has robbed many Calcuttans of the cashless facility that is often the difference between treatment and no treatment.

Patients with corporate insurance can still avail themselves of tension-free cashless treatment but the majority have little option other than to dig into their savings — or make a beeline for bank loans — with some of the top private hospitals either refusing to be part of or pulling out of an agreement with the conglomerate of public sector insurance companies.

Apollo Gleneagles, Belle Vue and Woodlands cite “unfeasible rates” offered by the insurers for refusing to be part of the agreement. CMRI had signed the pact but pulled out in January. Ruby might follow suit.

The Mediclaim quartet — National Insurance Company, New India Assurance, United India Insurance and Oriental Insurance — maintain that their rates are justified and meant to iron out “discrepancies in the billing process” at private hospitals.

Caught in this tug-of-war is the unsuspecting patient who pays his premiums regularly so that come sickness and the need for hospitalisation, money won’t be a hurdle.

Insurance agents, the only interface between the insurer and the insured, often conceal from their clients the crucial information that the top hospitals don’t offer cashless treatment any longer unless a person has corporate or private health insurance that costs way more. Many people learn during or after hospitalisation that they need to pay the hospitals from their own pockets and fight their battles for reimbursement with the public sector insurers later.

“In Calcutta, that translates into around 85 per cent of the people who have health insurance,” an insurance adviser said. “Mediclaim remains the preferred policy not only because it comes with the seal of government assurance and is cheaper but also because the public sector companies cover everyone from a three-month-old infant to an 80-year-old.”

Radha Chattopadhyay, a 55-year-old homemaker, got admitted to a private hospital in Alipore for hernia surgery recently, little knowing that her trusted cashless policy would become a problem.

“We had received cashless benefits several times earlier against this insurance policy. So we were confident there wouldn’t be any hassle this time too,” her husband Kamal Chattopadhyay, a doctor, told Metro.

Chattopadhyay was shocked when the hospital told him after his wife’s surgery that the cashless benefit of the insurance scheme was no longer available. “The package cost was Rs 1.1 lakh and I had to pay the entire amount myself. The insurance company later approved only Rs 36,000, that too after long-drawn negotiations,” he said.

The conglomerate of four public sector insurance companies, led by National Insurance, had approached private hospitals in the city with their Preferred Public Network (PPN) agreement in January 2012. The document included pricing fixed by the insurance quartet for 37 common procedures.

While 92 hospitals and nursing homes signed the agreement after mediation by third-party administrators, some of the big names such as Apollo Gleneagles Hospitals, Belle Vue Clinic, Bhagirathi Neotia Woman and Child Care Centre and Woodlands Multispeciality Hospital opted out and discontinued cashless benefits for patients with Mediclaim.

Sources said at least 3,600 patients didn’t get admitted to Apollo over the past year after learning that they wouldn’t get cashless insurance.

“We didn’t sign the agreement as the rates offered were almost half our existing prices. We submitted a discounted rate chart but the insurance companies have yet to agree,” said Rupali Basu, the CEO of Apollo Gleneagles.

Basu insisted it was difficult for private hospitals to provide “quality treatment” at prices offered by the insurers. Private health care providers also cite long credit periods and lack of transparency for turning their backs on cashless Mediclaim.

“We withdrew from the PPN agreement because the rates are very low overall and difficult to sustain. Also, since the agreement didn’t permit cashless benefit for patients opting for higher-priced single rooms, many were going to other hospitals,” said Rupak Barua, the COO of CMRI.

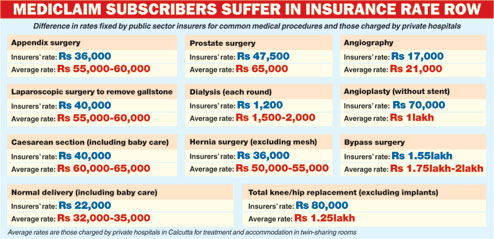

For an appendix surgery, the rate fixed by the public sector insurance companies is Rs 36,000. The average price of the procedure in private hospitals is between Rs 55,000 and Rs 60,000 (see chart).

Private hospitals also accuse the public sector insurers of delaying payments inordinately even after a claim has been submitted with bona fide documents.

“The insurers had promised us fast clearance of dues under the PPN agreement but that’s not happening. The credit period stretches up to a year in some cases, which causes severe inconvenience,” said S.B. Purkayastha, the CEO of Ruby General Hospital.

Other private hospitals are also unhappy with the rates but remain part of the PPN because opting out would mean losing a chunk of the patients.

“A lot of people depend on the cashless facility, so we are still providing the benefit. But the rates are unfair and these are different for different cities. Also, the operational costs such as power tariff and minimum wages have risen over the past year and must be taken into account,” said Alok Roy, the chairman of Medica Superspecialty Hospital.

Sources said some of the hospitals had signed the agreement with an eye on bulk occupancy. They soon found out that the rates were not viable. The occupancy rate didn’t go up either.

Many doctors are also reluctant to provide treatment under the PPN because of the low fees. “In specialised fields like oncology, it is not feasible to have a fixed rate for major surgeries where the condition of patients can turn critical and necessitate further intervention and therapy,” said surgical oncologist Gautam Mukhopadhyay.

For surgery to remove a lump in the breast, the public sector insurers have pegged the surgeon’s fees between Rs 5,000 and Rs 6,000. A surgeon attached to a private hospital usually charges between Rs 10,000 and Rs 15,000 for the procedure.

According to officials of the insurance companies, the rates were fixed after a series of discussions with officials of various hospitals and senior doctors. “Some didn’t agree and some requested a review of the rates, which we are trying to negotiate with the hospitals,” said a representative of National Insurance.

Another argument for a uniform rate is “huge discrepancy” in the rates of medical procedures at different hospitals. “The earlier rates had been fixed arbitrarily. We only wanted to regulate the billing process and so set a standard,” said Subir Bhattacharya, general manager of National Insurance.

As the impasse drags, more patients are being sucked into the vortex. Like Ila Mitra, who was billed Rs 3.5 lakh for bypass surgery recently and told she needed to clear the hospital’s dues before claiming insurance.

How has the impasse over cashless insurance affected you? Tell metro@abpmail.com