The recent RBI move to reduce the repo rate by 50 basis points is set to have serious repercussions for savers, beginning with an inevitable cut in interest rates on fixed deposits. This is likely to relegate FDs a few notches lower on the popularity charts, creating additional scope for investments in debt funds, the performance of which will depend on market conditions.

Small savings scare

Predictably, those who depend on small savings will be the worst-hit, given the kind of signals coming in the wake of the apex bank's announcement. Small savings instruments are prized by the masses. Countless savers depend on administered-rate schemes (such as post office deposits) to meet their monthly expenses. Any reduction in their rates will tilt the scales against them.

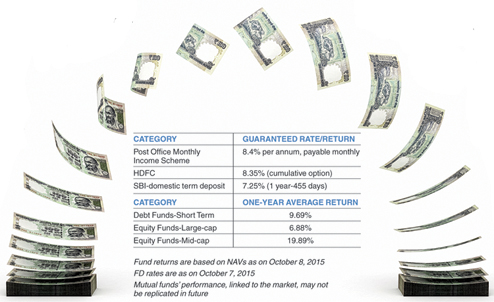

Postal deposits, which carry the hallmark of surety and certainty, are finely poised at the moment in terms of rates. The ubiquitous Post Office Monthly Income Scheme offers 8.4 per cent per annum, payable monthly. There are stringent limits, nevertheless, and these accounts cannot be opened just casually by individuals intending to deposit huge amounts in safe options.

In contrast, bank deposit rates have been pared already. The State Bank of India, the country's largest bank, now offers 7.25 per cent on domestic deposits (period: one year to 455 days). Other banks have followed suit. Depositors who wish to spread their money over multiple accounts will face the same trend everywhere.

Debt edge

Remember, declining interest rates are generally viewed as a positive development by debt afficionados. That is because of the inverse connection between rates and prices of debt securities. The two elements are known to move in opposite directions - when interest rates soften, prices of securities move north. At the end, mutual fund investors gain from the appreciation in net asset values.

It is too early to predict exactly how much the debt funds will gain on an average. However, there is sufficient historical evidence to suggest that at least longer-term funds have generated handsome returns when rates were cut. Chances are that history will be repeated.

Let's take a look at the returns generated in the recent past, say, over a twelve-month period. At least half a dozen funds have given well over 14 per cent in the past year, based on NAVs as on October 6, 2015. The average score - a little over 12 per cent - has also made these funds attractive.

Investors know they have a diverse range of debt funds before them. If you have, for instance, money to spare for only a year or so, you will simply need to locate a well-performing short-term fund. Here, your risk will be lower than those willing to stay invested for a longer duration, say, for three years. This diversity, and the fact that buying funds is an uncomplicated and trouble-free exercise, enhances their appeal.

Equity score

The central bank's move will have no direct fallout for equity funds. However, there are a few issues that followers of equities may want to know. If, for instance, the case for fixed income becomes perceptibly diluted, a section of the market is likely to gravitate to other asset classes.

As things stand, equity may end up as a clear winner. Yet, as all those who are familiar with economic fundamentals will agree that there are quite a few obstacles for equity funds at this juncture.

Not all global and local factors are conducive for stocks. The possibility of changes in US interest rates, for example, is expected to steer large-scale investments away from the Indian equity market. Locally, a number of major segments of the economy, such as commodities and energy, are under grave pressure. It remains to be seen how Indian stocks react to these challenges in the medium and long term.

It will be wrong to expect uniform returns from equity funds in the future - not when the mood is a little on the dull side. Equity funds mostly have had a fairly decent run in the recent past. Mid-cap funds, for example, have delivered an average 18.75 per cent in the past year. A section of the multi-cap funds, too, did discernibly well. But the score is decidedly lower for large-cap funds, which have provided a mere 5.93 per cent over the same period.

What should you do?

Here are a few points for you to consider before you work out your allocations.

- Take a hard look at FD rates, which will invariably fetch lower returns in the days ahead. Ask yourself: Will these rates be good enough for me? If the answer is negative, you will need to weigh other options.

- If you have the appetite for market-linked performance, debt funds may well be a friendly alternative. Consider your time horizon before you zero in on the kind of funds you want in your portfolio.

- Be aware of the risks. Returns are dependent on fund managers' ability to fight the odds - interest rate and credit risks will figure among the principal destroyers of wealth.

- If you can assume additional risks, a slight exposure to equity may be considered as well. For starters, hybrid funds can be explored. Consider funds that have mainly debt securities, with measured doses of equity serving. At the moment, monthly income plans (MIPs) combine both asset classes in their portfolios. However, remember MIPs do not guarantee any income (monthly or otherwise).

The author is director, Wishlist Capital Advisors