Mumbai: Analysts are sceptical of the measures announced by the Narendra Modi-government on Friday to check the slide in the rupee and rein in the current account deficit (CAD) and they fear the currency could again find itself exposed to the vagaries of the world markets after a two-day rally that saw the rupee gain 85 paise against the dollar.

However, the rupee will remain range-bound, amid the possibility of more measures from the Reserve Bank of India (RBI) and the Centre.

The government announced five measures on Friday that included the review of mandatory hedging condition for infrastructure loans.

It was decided to permit manufacturing entities to avail themselves the external commercial borrowing (ECB) facility with a minimum maturity of one year, instead of three years.

The Centre had also said it would remove the restriction on an FPI (foreign portfolio investment) to limit 20 per cent of its total investment in a single entity as well 50 per cent in a single corporate bond.

Further, with regard to rupee-denominated bonds, which is popularly known as masala bonds, the Centre has decided to do away with the withholding tax on these instruments till March 2019.

The government said the measures will bring additional capital flows of $ 8-10 billion, though analysts told The Telegraph that the effects would not be felt immediately.

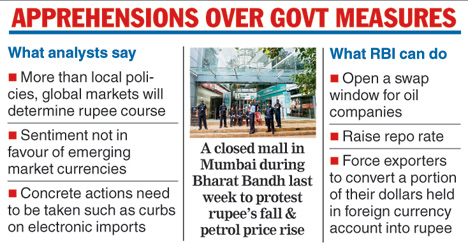

They said the measures would have worked, if the sentiment was in favour of the emerging markets.

"At first glance, the announcements by the finance minister fell short of expectations. At the core, given the deterioration in current account, we are borrowing fickle, expensive money to fund our oil and smartphone purchases.

"The finance minister also promised a review of non-essential imports and a filip to exports. While tariffs are not ideal, on balance some short-term steps to curb electronics demand may be appropriate," Ananth Narayan, professor at the SP Jain Institute of Management and Research, said.

Market circles are also expecting some action from the Reserve Bank to support the rupee.

These may include the opening of a swap window for oil companies.

A repeat of the step taken in 2012 where the central bank had asked exporters to convert a portion of their dollars held in their foreign currency account is also not ruled out. The RBI is widely expected to raise the policy repo rate by 25 basis points in its monetary policy due early next month.

Abheek Barua, chief economist at HDFC Bank, said the capital account measures announced on Friday were unlikely to result in any significant shift in fund flows. However, the governent's plan to curb imports may have some effect since it strikes at the heart of the current problem.

"This could mean that the rupee trajectory might not see a full reversal of the appreciation move of the last couple of days. That said, markets will wait for clarity on the specific items that face these curbs before give a thumbs-up to the rupee,'' he said in a note.

Barua further pointed out that the steps were better suited when the sentiment in the global market is positive towards emerging markets and when it is relatively easy for emerging market corporates to raise money abroad.

Some feel the steps taken by the government is suitable in the current context.

"We view the government's guarded response as appropriate because India's macro fundamentals are in a much better shape today than in 2013 - higher growth, stable inflation and fiscal commitment and do not necessitate a knee-jerk reaction'' Japanese financial services major Nomura said in a report.

However, additional capital inflows would continue to be determined by external factors rather than internal policies.