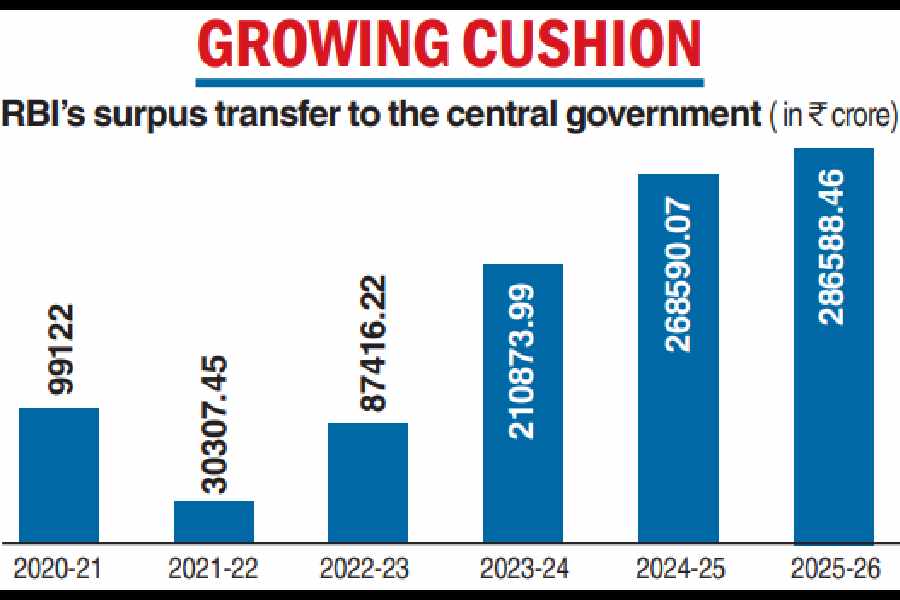

The Reserve Bank of India has raised its surplus transfer to the Centre to ₹2.86 lakh crore for the accounting year 2025-26, providing the government with additional fiscal space at a time when the economy is grappling with uncertainties arising from the West Asia crisis.

The dividend payout, which forms a key component of the Centre’s non-tax revenue, is higher than the record ₹2.68 lakh crore transferred in FY25. However, the transfer fell short of market expectations of around ₹3 lakh crore, prompting analysts to caution that the fiscal deficit could still overshoot the government’s target of 4.3 per cent of GDP for FY27.

The lower-than-expected payout also suggests the RBI has opted for a conservative stance amid heightened external risks.

The central bank maintained the contingency risk buffer (CRB) — a reserve retained to cushion against unforeseen financial and external shocks — at 6.5 per cent of the size of the balance sheet. It is near the upper end of the mandated 4.5-7.5 per cent range, indicating a preference to preserve buffers in an increasingly volatile global environment.

“Taking into consideration the current macroeconomic factors, financial performance of the bank and maintenance of appropriate risk buffers, the central board decided to transfer ₹1,09,379.64 crore towards the CRB for FY26 as against ₹44,861.70 crore in the previous year, and maintain the CRB at 6.5 per cent of the size of the RBI balance sheet,” a statement from the RBI said.

A lower CRB would have unlocked more surplus to be transferred to the government, which has budgeted a receipt of ₹3.91 lakh crore as dividend/surplus of RBI, nationalised banks and financial institutions in FY27.

Fiscal concern

The lower-than-expected dividend payout from the RBI has raised concerns over the Centre’s ability to meet its fiscal deficit target of 4.3 per cent of gross domestic product for FY27.

Economists said the smaller-than-anticipated surplus transfer could reduce the government’s fiscal flexibility at a time when higher global oil prices are already straining public finances.

The shortfall may compel the government to either curtail expenditure or raise additional borrowings, even as Prime Minister Narendra Modi has called for austerity measures and fuel conservation to protect foreign exchange reserves.

“The RBI surplus transfer is marginally lower than expected, thereby limiting the levers for the government in terms of managing the fiscal slippage risks,” said Upasna Bhardwaj, chief economist at Kotak Mahindra Bank. She added that while additional borrowing risks remain limited for now, the trajectory of subsidy expenditure and tax revenue growth will need close monitoring.

Dhiraj Nim, economist at ANZ Banking Group, said the fiscal deficit could widen to 4.6 per cent of GDP this fiscal against the budgeted 4.3 per cent if oil prices remain elevated.

Madan Sabnavis, chief economist at Bank of Baroda, said the RBI transfer was below expectations of ₹3-3.2 lakh crore and warned that rising fertiliser subsidies and lower contributions from oil marketing companies could further pressure the fiscal position.

Aditi Nayar of ICRA said the fiscal deficit could overshoot the target by 40 basis points if crude oil averages $95 per barrel during FY27.

Balance sheet grows

RBI’s balance sheet expanded by 20.61 per cent to ₹91,97,121.08 crore as on March 31, 2026. The central bank said that its net income, before risk provision and transfer to statutory funds, aggregated ₹3,95,972.10 crore in FY26, up from ₹3,13,455.77 crore in FY25.

RBI’s income comes from loans to commercial banks, interest on government securities, foreign exchange operations, including the buying and selling of dollars, seigniorage, and other fees and charges. Analysts said the central bank is likely to have booked substantial gains through active intervention in currency markets, particularly by selling dollars to curb excessive depreciation in the rupee.

However, the reduction in the CRB to 6.5 per cent in FY26 from 7.5 per cent a year ago has marginally lowered the cushion available to absorb mark-to-market losses arising from reserve deployment during periods of heightened volatility.

“The RBI’s ability to intervene in the rupee market is determined by the level of forex reserves and its institutional willingness to deploy them — both of which remain intact,” a senior banker told The Telegraph. “The dividend is essentially a distribution of profits already earned, including from the forex operations that form part of the defence mechanism.”

There are, however, concerns over the drawdown in foreign currency assets and the sizeable outstanding forward book, which could limit the RBI’s ability to sustain aggressive dollar sales if strength in the US currency persists.