These are gut-wrenching times for those who had in recent years scrambled to buy banking and financial services (BFS) stocks, many of which scaled the valuation charts only to bear the brunt of large-scale selling by investors, both institutional and retail. In a backdrop marked by inflationary pressures, a weakening rupee, the IL&FS-induced crisis and, of course, allegations against the banking regulator, the BFS sector clearly seems to be on the backfoot.

Even as investors hesitate to make fresh allocations to banks and finance companies, the one category which has been shaken quite severely is mutual funds. Equity funds with substantial exposure to the sector have already felt the heat. NAVs have dropped, a trend that is being partly attributed to the slowdown in the BFS space.

What will investors do in the present circumstances? Should they carry out a strategic retreat from the sector? What are the dos and don'ts for them? Let us consider some of these points here.

Source: NSE (Data as on September 28, 2018)

Clear trends

To recap quickly, BFS stocks account for a huge portion of allocations made by asset management companies. A number of funds have invested more than 20-25 per cent of their assets in them. While much of this is in favour of well-known banking and finance players, a sprinkling of smaller and relatively new outfits (such as insurance companies and new-generation loan providers) is also visible. together their overwhelming contribution to the portfolios is now a matter of concern.

The situation, quite predictably, is still evolving — it is a bit too early to suggest whether there is indeed a major liquidity crunch, and the probable impact of such a phenomenon on the financial markets. The scenario has already led to a perceived disagreement between the government and the banking regulator.

Be that as it may, if you are an ordinary investor with equity funds among your holdings, this is what you need to do:

- Check out the latest portfolios of your equity funds. These are easily available. Fund houses publish month-end statements regularly.

- Find out your funds’ current exposure to BFS. Is this an ungainly proportion of the overall holdings — ungainly enough to make you feel uncomfortable?

- Now, if the answer to the question raised above is not affirmative, there is scope for you to rationalise. You can do this by modifying your investments, and this plan can be executed in several ways.

- Whatever may be your modification plan, you must remember two critical issues: expenses and taxation. If these are spawned excessively because of your newly adopted policy, there is need for careful planning.

Strategic withdrawal

For the average investor, this may be far too early to consider a graded retreat from the sector. However, a watchful stand is absolutely necessary. In a backdrop marked by a systemic slowdown in the financial services space, a sharper downturn in BFS fortunes cannot be ruled out at this stage.

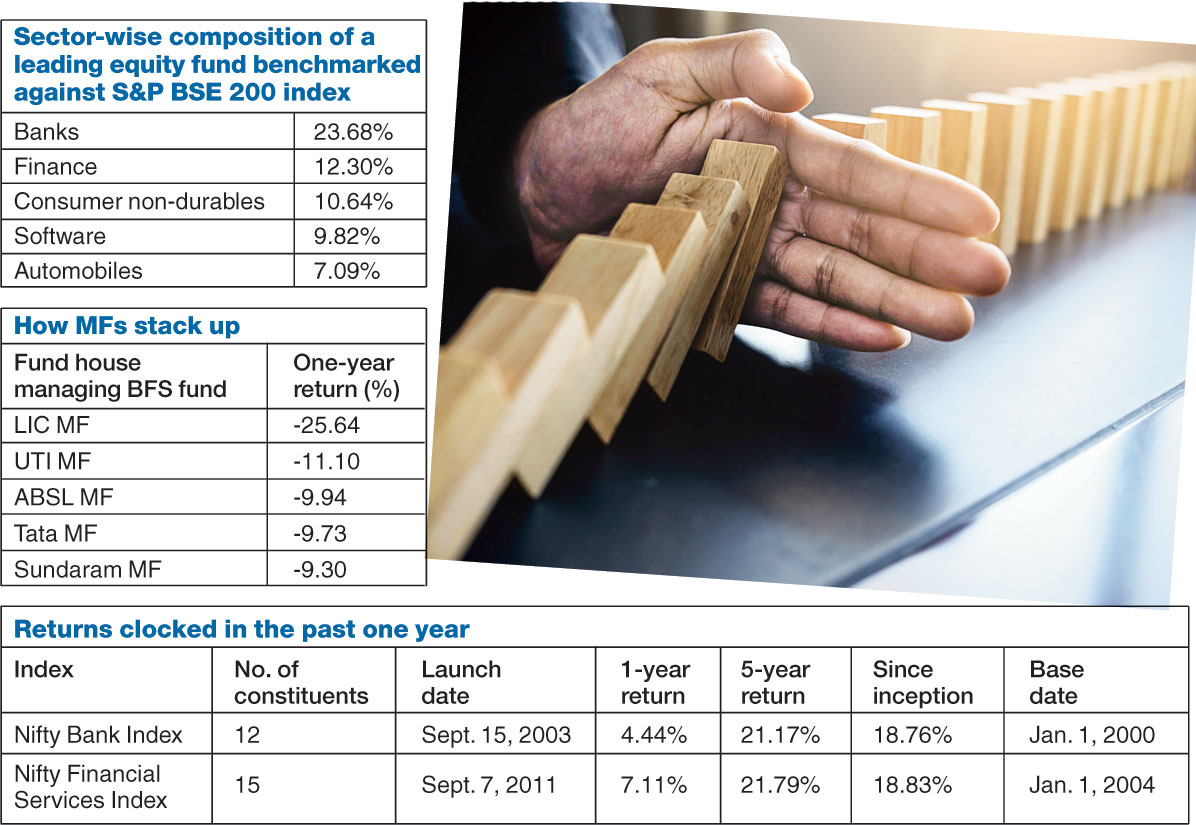

In such circumstances, one must underline the relative position enjoyed by bank-specific funds in recent years, several of which have done pretty well during select periods of growth. However, the last few months have been really bad for these funds, and the latest 52-week tally recorded by the laggards among them is particularly awful (See chart on mutual fund performance).

A calculated retreat — not an easy task to accomplish — may be necessary from banking funds. Sectoral plays are a lot riskier than diversified funds and investors must generally exercise extreme caution while making their allocations. For the BFS space, the cycle has turned for the worse and the best days seem to have passed. It is still a cycle, nevertheless — it will turn again, it is just a matter of time (See Chart 2 on indices performance).

An investor who moves out of BFS needs to find decent alternatives. You can gain by finding answers to the following posers: What will you do with the redemption proceeds? How will it be invested? More specifically, is there a case for parking the same in a liquid fund or a short-term debt fund for the time being? This will, after all, allow you to time a tactical allocation elsewhere.

Whether you like it or not, BFS is an extremely significant component of the economy. It accounts for a very substantial portion of the service sector’s productivity. No fund manager can afford to ignore it. However, adjustments in allocation patterns are well recommended in keeping with the changing views and latest trends. Investors at all times must remember that no allocation is sacrosanct. Clearly, modification is a sign progress.

The writer is director, Wishlist Capital Advisors